Buying an artificial intelligence (AI) stock that is trading at an attractive valuation and growing at an impressive rate may seem difficult right now, considering companies capable of leveraging this technology in the past have experienced a rapid rise in their share prices a year or so.

Nvidia, for example, trades at 71 times trailing earnings, although the good thing is that the chipmaker was able to justify its premium valuation with stellar growth. On the other hand, AI software plays a role Palantir Technologies is trading at an expensive valuation, but its growth hasn’t been enough to justify its high metrics.

However, investors looking for a mix of growth and value in the AI niche are in luck because there is one company – Taiwan semiconductor manufacturing (NYSE:TSM), popularly known as TSMC – which is currently not only cheap but also seems to be achieving impressive growth. Let’s look at why investors should consider buying this stock before it reports its first quarter 2024 results on April 18.

TSMC is expected to grow more than expected

When TSMC reported fourth-quarter 2023 results in January this year, the company forecast first-quarter 2024 revenue of $18.4 billion, at the midpoint of its range.

However, monthly sales statistics for the first three months of 2024 suggest that the company is on track to surpass that mark. More importantly, revenue growth has accelerated with each passing month.

In January, TSMC’s monthly revenue rose 8% year over year. This was followed by an 11% increase in February, while March was even better with a year-on-year increase of 34%. So first-quarter revenue was $18.86 billion, up nearly 14% year-over-year and above the consensus estimate of $18.26 billion.

Full quarterly results will be released on April 18, and it won’t be surprising if the stock sees a rise following the release. That’s because demand for AI chips in various applications is now having a greater impact for TSMC, as its March quarterly revenue shows us.

The long-term growth of the AI chip market will provide a tailwind for TSMC

Apple is TSMC’s largest customer, accounting for 25% of its revenue. But the smartphone maker is struggling to grow, as its latest results show us.

In addition, Apple will begin ramping up production of its iPhones, for which TSMC supplies chips, in the second half of the year. The chipmaker’s sharp increase in sales last month can be attributed to booming demand from companies like Nvidia. AMD, Intel, QualcommAnd Broadcomwho are among the seven largest customers.

All of these chipmakers are focused on delivering new AI chips as well as increasing production of their existing products to meet strong customer demand. For this reason, TSMC has rapidly increased its production capacity. The company is expected to double its advanced chip packaging capacity to 240,000 wafers this year from 120,000 wafers last year, largely due to demand from Nvidia, which accounts for an estimated 60% of its advanced chip manufacturing capacity .

Intel, on the other hand, recently unveiled a new AI accelerator called Gaudi 3, based on TSMC’s 5-nanometer manufacturing process. Intel has already started shipping samples of this chip and expects full production in the third quarter of 2024. Meanwhile, interest in Broadcom’s custom AI processors is increasing, and the company also recently signed a new customer.

Likewise, Qualcomm is well on its way to benefiting from the increasing adoption of AI in smartphones and PCs. Overall, TSMC is in an excellent position to benefit from the long-term growth of the AI chip market, especially considering that it is the world’s leading semiconductor manufacturer with an estimated 61% market share. This is significantly higher than second-place Samsung’s share of 11%.

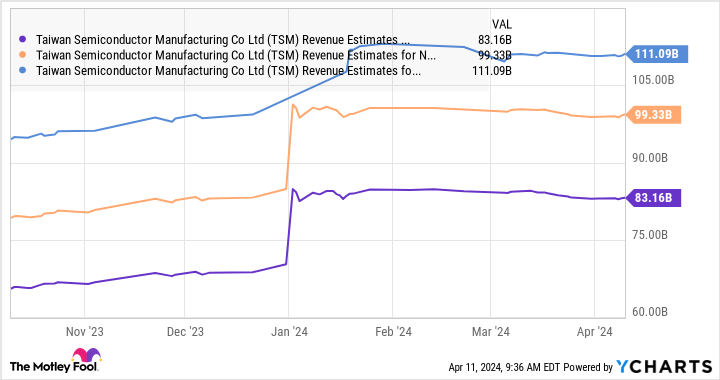

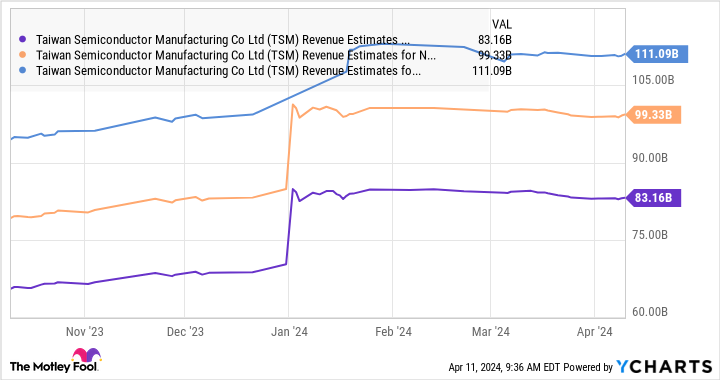

Considering that the global AI chip market is expected to grow 38% annually through 2032, there’s a good chance that TSMC will maintain its impressive momentum. The chart below suggests that analysts expect strong sales increases in 2024 and beyond compared to last year’s sales of $69.3 billion.

Therefore, buying this semiconductor stock seems like a no-brainer at this point given its attractive valuation. TSMC trades at 29 times trailing earnings, a discount to that Nasdaq 100The earnings multiple of 30 (using the index as a proxy for technology stocks). The expected earnings multiple of 24 is also lower than the Nasdaq 100 value.

Additionally, TSMC shares are significantly cheaper than Nvidia, meaning it’s a more cost-effective way to capitalize on the AI chip boom.

The above evidence also shows that TSMC appears to be poised for long-term growth given its critical role in the AI chip market, which is why investors would do well to buy this AI stock before jumping past its 40 percent price the heights skyrocket (and become expensive). Increases it has recorded so far in 2024.

Should you invest $1,000 in Taiwan Semiconductor Manufacturing now?

Before buying Taiwan Semiconductor Manufacturing stock, consider the following:

The Motley Fool Stock Advisor The analyst team has just identified what they think this is The 10 best stocks so investors can buy it now… and Taiwan Semiconductor Manufacturing wasn’t one of them. The ten stocks that made the cut could deliver huge returns in the years to come.

Think about when Nvidia created this list on April 15, 2005… if you have $1,000 invested at the time of our recommendation, You would have $540,321!*

Stock Advisor provides investors with an easy-to-follow roadmap to success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks per month. The Stock Advisor has service more than quadrupled the return of the S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns from April 8, 2024

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Apple, Nvidia, Palantir Technologies, Qualcomm and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Broadcom and Intel and recommends the following options: long January 2023 $57.50 calls on Intel, long January 2025 $45 calls on Intel, and short May 2024 $47 calls on Intel . The Motley Fool has a disclosure policy.

1 Cheaply Rated Artificial Intelligence (AI) Stock to Buy Hands-On Before April 18 was originally published by The Motley Fool