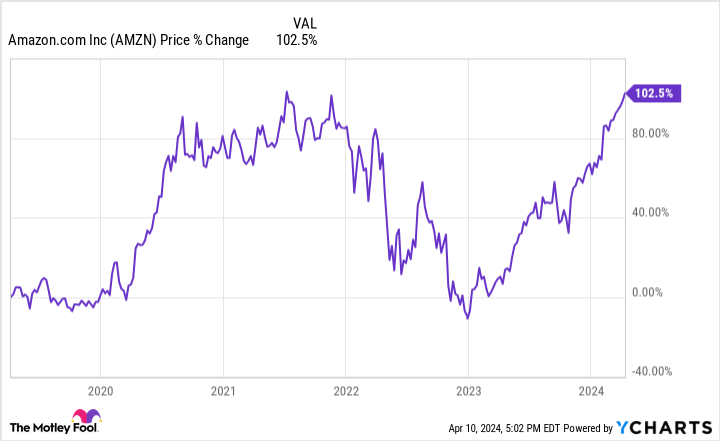

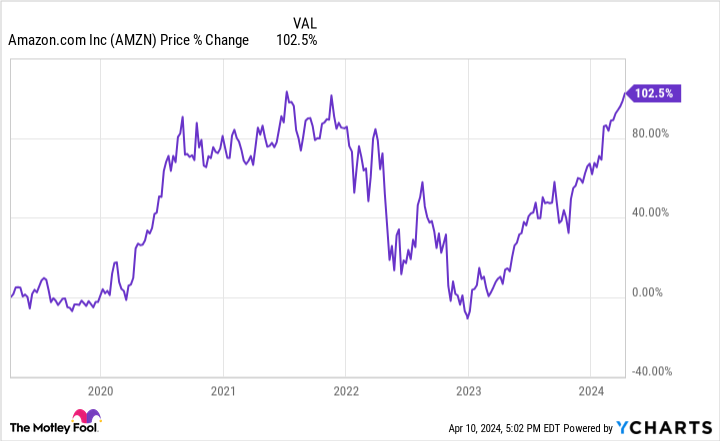

The last few months have been positive for shareholders Amazon (NASDAQ:AMZN). The stock is up 45% in the last six months and 22% year-to-date.

With a market cap of $1.93 trillion, shares recently surpassed all-time highs reached in 2021 as investors grew concerned about the profitability of e-commerce businesses and resurgent growth in cloud computing due to the recent boom in artificial intelligence (AI). ) are becoming more and more optimistic.

Amazon stock is up 100% in the last five years. But what do the next five years look like? Can it repeat this outstanding performance and double it again? Let’s take a look.

Profit turnaround in e-commerce, further growth is imminent

Even though the online store has been around for almost 30 years, Amazon’s e-commerce and global retail operations are still growing quickly. North American sales rose 12% to $353 billion in 2023, while international operations grew 11% to $131.2 billion.

Despite Amazon’s platform being so dominant in the e-commerce sector, online shopping now accounts for only an estimated 15.6% of retail sales in the United States. If this number can continue to rise over the next 10 to 20 years and Amazon can maintain its market share, there are still many years left to grow sales.

The best part about this growth in Amazon’s e-commerce division is where it’s coming from. Third-party services rose 19% year-over-year last quarter and advertising services rose 26%. These high-margin segments can increase overall profit margins if they continue to grow rapidly.

And that’s exactly what we’re seeing today. Operating margins in North America reached 6.1% in the fourth quarter of 2023, increasing in each of the last six quarters and reversing from negative 0.3% in the fourth quarter of 2022. In 2024, investors should expect e-commerce profit margins to continue to increase.

A recovery of cloud computing

The company’s most profitable segment is its cloud computing division, Amazon Web Services (AWS). In 2023, the company generated revenue of over $90 billion and operating income of $24.6 billion, representing a profit margin of 27.1%.

However, there were major concerns about a slowdown in AWS in late 2022 and early 2023. Revenue growth fell from 28% in the third quarter of 2022 to 12% in the second quarter of 2023 as the company helped its software customers cut costs after the peak of the pandemic.

Today, these concerns have proven to be too pessimistic. AWS revenue accelerated to 13% growth in the fourth quarter, driving the stock higher. And revenue for 2024 and 2025 looks promising given the rapid rise of AI services. These new products use a lot of cloud computing to operate, and AWS wants to be one of the leaders in this space alphabetis Google Cloud and Microsoft Azure blue. For example, the company has signed an extensive agreement in this area with the fast-growing start-up Anthropic.

Analysts expect cloud computing to continue to grow over the next decade and beyond, with double-digit annual growth rates. If Amazon can maintain its market leadership as it has in e-commerce, AWS should have many more years of growth ahead of it.

Where will Amazon stock be in five years?

To estimate where the stock will be in five years, we need to make some earnings estimates for both E-Commerce and AWS. Let’s assume that e-commerce – excluding the unprofitable international segment – can increase sales by 12% annually over the next five years and increase profit margins to 10%. This would put North American retail profits at $62 billion in 2028.

Let’s assume the same for AWS and assume five years of 12% growth and a profit margin of 27%. In 2028, that would equate to AWS profits of $43 billion. Adding both numbers together gives Amazon a profit of $105 billion in 2028, not counting any upside from other businesses like international e-commerce or satellite internet services.

Now comes the hardest part: what profit multiple will Amazon trade at in 2028? An exact answer is impossible, but with a large competitive advantage in both cloud computing and e-commerce, I think the stock deserves to be traded at a market-beating multiple of 30x earnings, also known as price-to-earnings -Ratio to be traded (SPORT).

Multiply $105 billion by 30 and you get a market cap of $3.15 trillion, or a 66% increase from today’s price. While it’s not a doubling, it looks like Amazon still has upside potential for shareholders who stick around for the long haul.

Should you invest $1,000 in Amazon now?

Before you buy stocks on Amazon, consider the following:

The Motley Fool Stock Advisor The analyst team has just identified what they think this is The 10 best stocks so investors can buy it now… and Amazon wasn’t one of them. The ten stocks that made the cut could deliver huge returns in the years to come.

Think about when Nvidia created this list on April 15, 2005… if you have $1,000 invested at the time of our recommendation, You would have $540,321!*

Stock Advisor provides investors with an easy-to-follow roadmap to success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks per month. The Stock Advisor has service more than quadrupled the return of the S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns from April 8, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Brett Schafer holds positions at Alphabet and Amazon. The Motley Fool has positions in and recommends Alphabet, Amazon and Microsoft. The Motley Fool recommends the following options: long $395 January 2026 calls on Microsoft and short $405 January 2026 calls on Microsoft. The Motley Fool has a disclosure policy.

Where will Amazon stock be in 5 years? was originally published by The Motley Fool