Since Warren Buffett took over Berkshire Hathaway (NYSE:BRK.A) (NYSE:BRK.B) In 1965, the multinational holding company achieved a remarkable compound annual growth rate of 19.8% through 2023, nearly doubling the benchmark S&P 500The total return of 10.2% over the same period.

Given the unprecedented returns, it’s always wise to check Berkshire’s current holdings to find out which stocks the Oracle of Omaha thinks are worth owning. Here are three tips that align with Buffett’s timeless investing principles and show shareholders long-term potential.

1. American Express

American Express is a Buffet favorite and accounts for nearly 10% of Berkshire’s stock portfolio. Buffett’s first investment in the payments and credit card company dates back to 1991 and has since produced remarkable returns, increasing in value from $1.3 billion to about $35.5 billion. Notably, the increase in value does not include dividends, which were originally at $41 million per year and are estimated to be $409 million in 2024.

With returns like these, some investors might think American Express’s best days are over, but there’s still a lot that’s good about the company. First, American Express recently reported revenue of $15.8 billion and diluted earnings per share (EPS) of $3.33 for the first quarter of 2024, up 11% and 39%, respectively, year-over-year corresponds. Management reiterated its optimistic outlook for 2024, including revenue growth between 9% and 11% and diluted EPS growth of 13% to 17%, which, if realized, would reach record highs.

American Express operates differently than its competitors, MasterCard (NYSE: MA) And Visas (NYSE:V), by acting as a closed network by issuing cards, granting loans to card users, and holding the loans on its books. This may result in higher merchant fees and annual fees for cardholders. This leaves the company more vulnerable to default and must record a non-cash expense, known as a provision for credit losses, for any expected losses that are unlikely to be recoverable over the next year. As high interest rates weigh on some businesses and consumers, this metric is rising for American Express, reaching $1.3 billion in the first quarter of 2024, up 18% year over year.

Nonetheless, American Express has $5.4 billion in net cash on its balance sheet, and its management is committed to returning capital to shareholders. Additionally, the company has paid a dividend since 1989, currently the quarterly dividend is $0.70 per share, which represents an annual yield of 1.2%. While American Express doesn’t always increase its dividend every year, Buffett noted in his 2022 annual letter to shareholders that he expects the dividend “will most likely increase.”

Finally, American Express management is conducting an aggressive share repurchase, reducing outstanding shares by nearly 14% over the past five years, and the board has the authority to repurchase an additional estimated 95 million shares from the current 719 million. To quote Buffett again: “The math is not complicated: as the number of shares decreases, your interest in our many companies increases.”

2. Mastercard

The second Berkshire stock you should add to your portfolio is another payments giant: Mastercard. As of Dec. 31, Berkshire held nearly 4 million shares. Berkshire’s holdings in Mastercard and Visa were initiated by its portfolio managers Todd Combs and Ted Weschler, not Buffett. But Buffett remarked at one of Bershire’s annual meetings: “I could have bought them, and in retrospect I would have.”

Mastercard is the second-largest payments processor by market cap at $432 billion and has narrowly beaten the S&P 500’s total return over the past five years, 95% versus 87%.

Mastercard, like Visa, operates as an open-loop network: every time a cardholder pays with a Mastercard, it charges a fee, even though the bank that issued the card has the credit. Mastercard generated $25.1 billion in revenue over the past 12 months and posted a five-year compound annual growth rate of 10.9%, beating Visa’s 9.6%. This higher compound annual growth rate also contributes to Mastercard’s higher valuation, with a price-to-earnings (P/E) ratio of 39 compared to Visa’s 32. And despite elevated interest rates, consumer spending is healthy, according to Mastercard Chief Financial Officer Sachin Mehra. In its last earnings call, the company noted that “consumer spending continues to be supported by a strong labor market and wage growth.”

Beyond its financials, Mastercard has paid a quarterly dividend since going public in 2006 and has increased it for the past 13 consecutive years. Today, Mastercard pays a quarterly dividend of $0.66 per share, representing an annual yield of 0.6%. Additionally, management repurchased $9 billion worth of shares in 2023 and reduced shares outstanding by 8.7% over the past five years.

3. Visa

If you haven’t noticed a theme yet, it should be clear with the latest Berkshire stock: Visa. The company, with a market capitalization of $562 billion, is the leader in the consumer payments market with 4.4 billion cards issued and generated revenue of $33.4 billion and net income of $18 billion in the last 12 months.

Like its competitors, Visa rewards shareholders with dividends and stock buybacks. First, Visa currently pays a quarterly dividend of $0.52 per share, which represents an annual yield of about 0.8%. The payments giant has increased its dividend for the 15th year in a row, putting it at the top of its peers in this category. Next, the company repurchased $2.7 billion of shares last quarter, leaving $23.6 billion in approved funds for share repurchases.

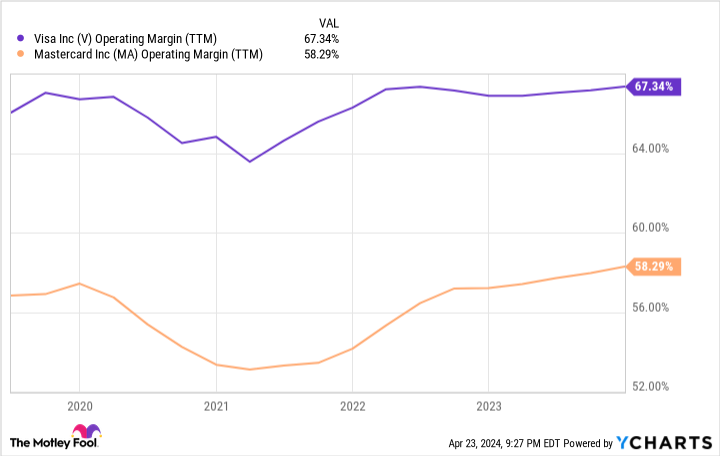

What sets Visa apart from its direct competitor, Mastercard, is its operating margin – a percentage of sales that a company retains as operating profit. Visa’s operating margin over the last 12 months was 67.4%, significantly higher than Mastercard’s over the same period (58.3%). In other words, Visa is more efficient at converting revenue into profit than Mastercard. As mentioned, Visa trades at a lower P/E than Mastercard, making the stock more valuable.

One area to keep an eye on with Visa is the growth in overall payment volume – or the number of transactions. Management recently lowered its estimate for fiscal 2024 from low double-digit percentages to high single-digit percentages compared to fiscal 2023, blaming slower-than-expected travel volumes in Asia Pacific.

The slight downgrade could be due to higher interest rates for consumers. Nonetheless, Visa CFO Chris Suh remains positive, recently stating, “Our data does not indicate a meaningful behavioral change across consumer segments.”

Are these three Warren Buffett stocks worth buying?

Buffett once said, “Payments are a huge deal around the world,” which is reflected in Berkshire’s portfolio of these three stocks. Given Berkshire Hathaway’s public filings, we can see that the most prominent and longest bet is on American Express, with a $35 billion stake. But as an investor, you don’t have to choose just one. In Visa’s most recent earnings call, management said the company’s total addressable market is $20 trillion, meaning there’s plenty of room for growth. Considering they are the three largest companies in the payments industry today, there is no reason not to buy all three.

Should you invest $1,000 in American Express now?

Before you buy American Express stock, consider the following:

The Motley Fool Stock Advisor The analyst team has just identified what they think this is The 10 best stocks so investors can buy it now…and American Express wasn’t one of them. The ten stocks that made the cut could deliver huge returns in the years to come.

Think about when Nvidia created this list on April 15, 2005… if you have $1,000 invested at the time of our recommendation, You would have $506,291!*

Stock Advisor provides investors with an easy-to-follow roadmap to success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks per month. The Stock Advisor has service more than quadrupled the return of the S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns from April 22, 2024

American Express is an advertising partner of The Ascent, a Motley Fool company. Collin Brantmeyer has held positions at American Express, Berkshire Hathaway, Mastercard and Visa. The Motley Fool has positions in and recommends Berkshire Hathaway, Mastercard and Visa. The Motley Fool recommends the following options: long January 2025 $370 calls on Mastercard and short $380 January 2025 calls on Mastercard. The Motley Fool has a disclosure policy.

3 Obvious Warren Buffett Stocks to Buy Now was originally published by The Motley Fool