It seems like higher inflation just won’t go away these days. The latest Consumer Price Index (CPI) report showed prices rose 3.5% year-on-year. This was higher than expected and showed an acceleration in price growth. Inflation continues to exceed the Federal Reserve’s target of around 2% per year.

While higher inflation is bad for the economy as a whole, it can benefit certain companies. Brookfield Renewables (NYSE:BEP)(NYSE:BEPC), Brookfield Infrastructure (NYSE:BIPPC)(NYSE:GDP)And Marathon Petroleum (NYSE:MPC) These three Motley Fool contributors stand out for their ability to benefit from higher inflation. It gives these energy stocks the fuel to pay higher dividends and provide their investors with income streams that beat inflation.

An inflation-driven boom

Matt DiLallo (Brookfield Renewables): While increased inflation is a challenge for many companies, it is a blessing for Brookfield Renewable. The renewable energy producer sells 90% of the electricity generated under fixed-price contracts with an average remaining term of 13 years. These arrangements provide the company with very predictable cash flow.

Most of these contracts contain clauses that link interest rates to inflation (70% of revenues are linked to inflation). This stable and constantly increasing cash flow puts the high-yield dividend (most recently over 6%) on a very solid foundation.

Brookfield expects increases in inflation to result in 2% to 3% annual growth in its operating funds (FFO) per share over the next five years assuming moderate inflation. However, higher inflation could result in annual FFO per share growth of up to 4% in the near term.

Inflation isn’t Brookfield Renewable’s only growth driver. The Company expects margin improvement activities (e.g., providing ancillary services and achieving higher market prices for its non-contracted production) and its extensive development pipeline to continue to drive 5% to 9% annual FFO per share growth become.

In addition, merger and acquisition activity is likely to provide further impetus. The company expects these catalysts should allow it to grow its FFO per share by more than 10% annually through at least 2028.

Brookfield’s growth drivers should provide sufficient strength to further increase its high-yield dividend. The company aims to increase its distribution by 5 to 9% annually. This should allow it to achieve income growth above inflation in the coming years, even if inflation remains high.

Built for every economy

Jason Hall (Brookfield Infrastructure): It may seem unoriginal that my colleague Matt and I chose two subsidiaries of the same parent company. But they are significantly different from each other, but also similar in the way that is most important in answering that call.

With Brookfield Infrastructure, you get a collection of world-class assets that connect the modern world, including energy (transportation and storage of electricity, natural gas and other raw materials), data (data centers, broadband and Wi-Fi), and people transportation and goods.

Investors looking to both reduce the impact of inflation and potentially benefit from it should consider this deal. First of all, its infrastructure assets are crucial regardless of the economic situation. Even as stubborn inflation weighs on capital investment and consumer spending, working capital will continue to be stretched and generating plenty of cash.

And many of the pricing structures of its assets take inflation into account, giving it the ability to increase the prices it charges as inflation rises higher and higher. But at the same time the operating costs are wide fewer affected by inflation. While its fixed costs are high, the variable aspects of its operations do not exactly follow inflation. This means investors are left with more cash flow.

But the market’s misunderstanding of the business has caused its share price to fall over the past year, largely due to concerns about rising interest rates. This allows smart investors with a long time horizon to buy this company at what I believe is the most attractive valuation in years.

With a dividend yield well above 5% and a strong track record of increasing payouts and delivering high returns over the last two decades, I think now is exactly the right time to buy Brookfield Infrastructure.

Stay ahead of inflation with one of the fastest-growing dividends in the energy sector

Tyler Crowe (Marathon Petroleum): One misconception about investing to ward off inflation is betting on high-yield stocks. While these now offer large cash payments, higher yielding stocks tend to grow their payouts more slowly. Often these rates are slower than inflation.

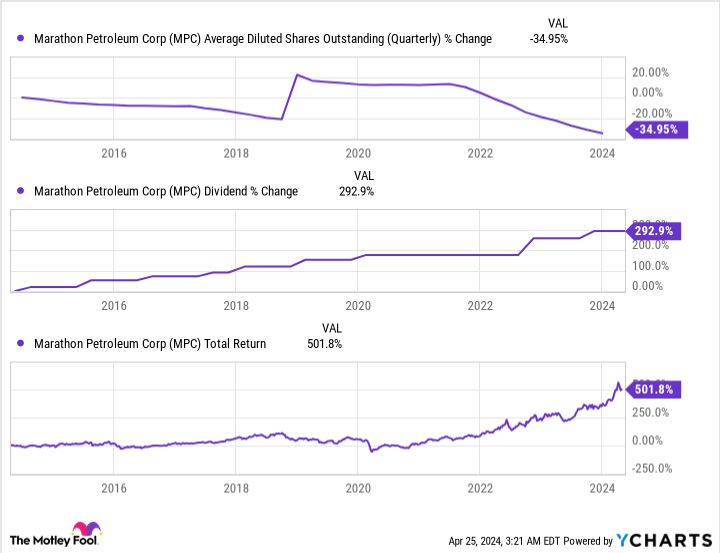

So instead of looking for high yields, investors are probably better off looking for dividend payers that have a long track record of growing their payouts at a high rate. Over the past 10 years, only 25 companies in the energy sector have increased their growth by 10% or more. Marathon Petroleum is one of them, increasing its payout by 14.6% annually over this period.

A rapidly growing dividend in a growthless industry like oil refining seems counterintuitive. However, with few opportunities to invest in growth, Marathon returns essentially all of its free cash flow to investors through dividends and share repurchases.

Over the last 10 years, the company has reduced its outstanding shares by 35% (including a significant all-stock acquisition in 2019). A lower share count means the company can pay higher dividends per share without spending more money each quarter.

Demand for refined petroleum products is likely to remain high over the next few decades, providing the company with ample opportunity to shower investors with further dividend payments and buybacks. If you want to beat inflation, few stocks will do it better than Marathon Petroleum.

Should you invest $1,000 in Brookfield Renewable now?

Before you buy shares of Brookfield Renewable, consider the following:

The Motley Fool Stock Advisor The analyst team has just identified what they think this is The 10 best stocks so investors can buy it now… and Brookfield Renewable wasn’t one of them. The ten stocks that made the cut could deliver huge returns in the years to come.

Think about when Nvidia created this list on April 15, 2005… if you have $1,000 invested at the time of our recommendation, You would have $506,291!*

Stock Advisor provides investors with an easy-to-follow roadmap to success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks per month. The Stock Advisor has service more than quadrupled the return of the S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns from April 22, 2024

Jason Hall holds positions at Brookfield Infrastructure, Brookfield Infrastructure Partners, Brookfield Renewable and Brookfield Renewable Partners. Matt DiLallo holds positions at Brookfield Infrastructure, Brookfield Infrastructure Partners, Brookfield Renewable and Brookfield Renewable Partners. Tyler Crowe holds positions at Brookfield Infrastructure Partners and Brookfield Renewable. The Motley Fool has positions in and recommends Brookfield Renewable. The Motley Fool recommends Brookfield Infrastructure Partners and Brookfield Renewable Partners. The Motley Fool has a disclosure policy.

Inflation Won’t Go Away: 3 Dividend Stocks to Cash In With was originally published by The Motley Fool