In the current bull market, a handful of technology companies are dominating events on Wall Street. This group became known as the “Magnificent Seven.” In 2024, some of these seven names will fall behind. Today, the remaining resilient high-flyers – Nvidia, Amazon, MetaplatformsAnd Microsoft – are referred to by some as the “Fab Four.”

Now may not be the time to continue betting on the few winners. After all, they are already sitting on huge profits. Instead, three Motley Fool contributors think you might want to consider shaking things up with a fallen angel like him Tesla (NASDAQ:TSLA)an up-and-coming guy CrowdStrike (NASDAQ:CRWD)or even a lottery ticket-like stock such as lemonade (NYSE:LMND).

AI could send struggling Tesla shares into overdrive

Will Healy (Tesla): One way to find affordable artificial intelligence (AI) stocks is to look for companies that have fallen out of favor for reasons other than their AI connections. This description fits Tesla. The company sold about 11% fewer electric vehicles (EVs) than it built in the first quarter, and rumors that it had abandoned plans for a cheaper Model 2 also weighed on the stock.

In fact, electric vehicle sales could continue to decline in the near term. However, Tesla has recently made improvements to its AI-powered fully self-driving platform, and CEO Elon Musk has announced that he will unveil his robotaxi on August 8th. Cathie Wood’s Ark Invest paid particular attention to the prospects inherent in this robotaxi based on its forecast that Tesla shares will reach $2,000 by 2027.

Ark Invest views Tesla as a robotics stock and expects the robotaxi to boost both sales of Tesla vehicles and the software-as-a-service platform that powers the robotaxi. The investment firm expects robotaxis to account for 67% of the company’s expected enterprise value by 2027. That would change the company dramatically, as automobile sales accounted for 85% of its revenue in 2023.

But given the target increase in the share price by more than tenfold by 2027, many investors are skeptical. However, it’s worth noting that in 2018, Ark Invest predicted that Tesla stock would reach $267 per share by 2021. This forecast also assumed an almost tenfold increase at the time – and it came true in the 2021 bull market.

Even if Ark Invest’s optimistic forecast falls short of expectations, investors have some cushion. After the recent selloff, Tesla’s P/E ratio is around 40 – near a record low for the stock.

Ultimately, this valuation is likely to rise, assuming a robust robotaxi platform significantly increases sales and profits. Therefore, Tesla could experience a massive upswing if it independently works its way back into investor portfolios.

CrowdStrike is on the cusp of great things

Jake Lerch (CrowdStrike): CrowdStrike is a leading provider of cybersecurity solutions – an area of growing importance given the seemingly endless number of cyberattacks the world continues to experience. Consider just one – the Change Healthcare hack that has crippled claims payments for tens of thousands of healthcare providers in recent weeks. Many companies are aware of the high costs of falling victim to such cyberattacks and are therefore looking to strengthen their digital defenses.

CrowdStrike, whose software relies on machine learning to monitor customer networks and identify suspects before damage is done, is quickly gaining new customers.

In its most recent fiscal quarter (ended January 31), CrowdStrike’s revenue increased 33% year-over-year to $845 million. Additionally, $796 million of that, or 94%, came from subscription revenue. This is important because subscription revenue is recurring and therefore more predictable than traditional sales, which tend to have larger ups and downs.

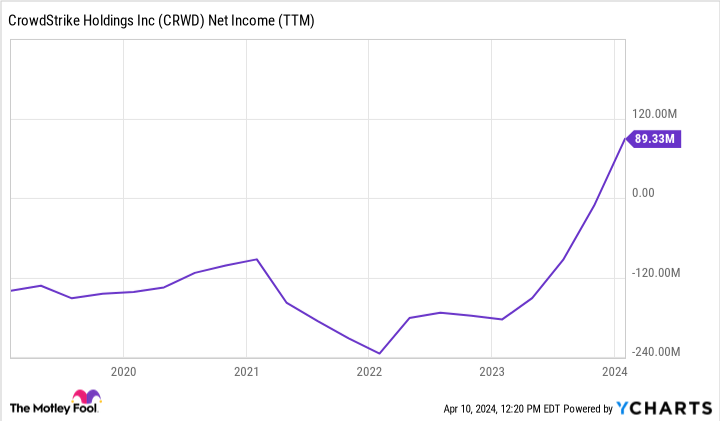

Additionally, CrowdStrike is making an important transition in its lifecycle: it is becoming profitable. Net profit was recently positive for the first time. The company generated a net profit of $89 million in the last 12 months. Additionally, free cash flow increased to $3.81 per share. This is crucial because increasing free cash flow per share is cited by many as the ultimate financial measure of a publicly traded company’s success – and is often correlated with long-term share price gains.

In short: CrowdStrike is the best of both worlds. It is a young company with growing free cash flow that is making the transition to consistent profitability. There is also a secular growth trend as more companies upgrade and strengthen their cyber defenses in the face of increasing threats. For these reasons, it’s a stock worth considering.

Lemonade’s AI offers a new twist on insurance

Justin Pope (Lemonade): Insurance is an ancient industry ripe for disruption. The incumbents – the giant insurance companies whose names you know, who all make commercials with professional athletes, funny mascots and recognizable spokespeople – are using AI to analyze data. However, they still sell policies through an agent model, which has given Lemonade ample opportunity to penetrate the market. Lemonade uses AI chatbots to communicate with customers and process claims. These bots can complete tasks in just 90 seconds and settle a claim in under three minutes. You may find yourself on hold longer waiting to speak with a representative from a traditional insurance company.

Lemonade’s app-first experience has won over many customers. Subscriber numbers rose 12% year-over-year to more than 2 million in the fourth quarter, a growth rate that suggests some people are leaving other insurance providers and switching to Lemonade. The product range is not yet as comprehensive as that of more established competitors, but customers can purchase rental, homeowners, auto, pet and life insurance here.

Insurance companies make a profit when they pay out fewer total claims than customers pay in total premiums. Lemonade is not yet profitable. However, non-GAAP EBITDA losses in the fourth quarter were $29 million, a 44% smaller loss than the year-ago period. Importantly, Lemonade has $945 million of cash on the books and generated positive cash flow in the second half of last year. This is a good sign that it is financially stable.

Lemonade is a risky investment at this point – for the company to be successful, it must continue to attract customers and find a way to become profitable. However, higher risk also means more opportunity for higher returns, and Lemonade, with its $1.2 billion market cap, could transform the portfolio if it can emerge as a major player in the insurance space.

Where can you invest $1,000 now?

When our team of analysts has a stock tip, it might be worth listening. After all, the newsletter they have been publishing for two decades is Motley Fool Stock Advisorhas more than tripled the market.*

They just revealed what they think it is The 10 best stocks for investors to buy now… and Tesla made the list – but there are 9 other stocks you might be overlooking.

Check out the 10 stocks

*Stock Advisor returns from April 8, 2024

Randi Zuckerberg, former director of market development and spokesperson for Facebook and sister of Mark Zuckerberg, CEO of Meta Platforms, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Jake Lerch has positions at Amazon, CrowdStrike, Nvidia and Tesla. Justin Pope has no position in any of the stocks mentioned. Will Healy holds positions at CrowdStrike. The Motley Fool has positions in and recommends Amazon, CrowdStrike, Lemonade, Meta Platforms, Microsoft, Nvidia and Tesla. The Motley Fool recommends the following options: long $395 January 2026 calls on Microsoft and short $405 January 2026 calls on Microsoft. The Motley Fool has a disclosure policy.

Forget the Fab Four: These 3 Artificial Intelligence (AI) Stocks Are Great Buys Today was originally published by The Motley Fool