Bond king Bill Gross may be best known for his fixed income investing acumen, but the billionaire recently posted on X, formerly known as Twitter, that he loves master limited partnership (MLP) pipeline stocks. He named three high-yielding stocks in particular.

Let’s take a look at the MLP stocks Gross is a fan of and why they could be attractive investments.

MPLX

There are many things to like MPLX (NYSE:MPLX)which is approximately 65% owned by the refinery Marathon Petroleum (NYSE:MPC).

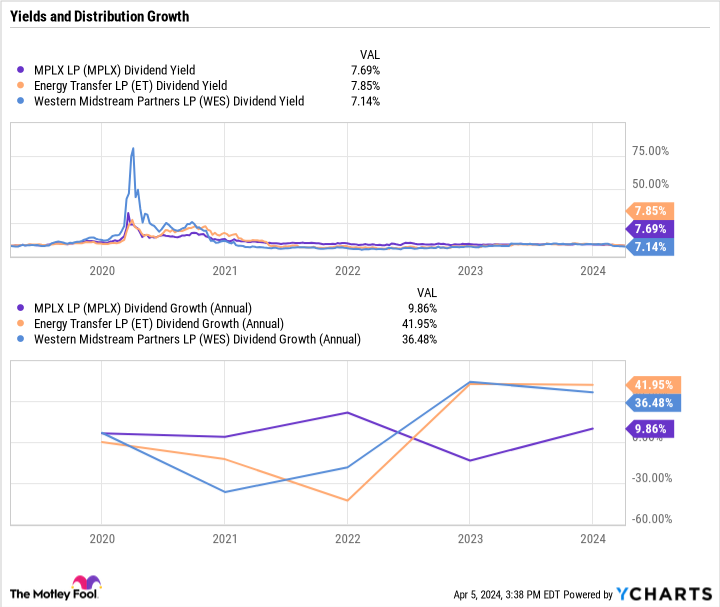

One of MPLX’s most attractive features is its current 7.7% yield and increasing distribution. MPLX increased its distribution by 10% in 2023 and is poised to increase it this year as well. The company also has a strong balance sheet with 3.3x leverage and a payout-to-coverage ratio of 1.6. Leverage for MPLX is consolidated net debt divided by trailing twelve-month adjusted earnings before interest, taxes, depreciation and amortization (EBITDA). The coverage ratio, in turn, is the cash flow divided by the distribution. Medium-sized companies typically aim for leverage between 3.0x and 4.0x. A coverage ratio greater than 1.0x means that a company’s distribution is currently covered by its cash flow.

MPLX’s logistics and warehousing segment, which accounts for approximately two-thirds of Adjusted EBITDA, has attractive long-term, fee-based contracts with Marathon, which typically include minimum volume commitments. Therefore, the segment tends to have a stable performance with high visibility. Its gathering and processing segment is more tied to natural gas volumes from the Marcellus and Utica Shales, two of the lowest-cost natural gas basins in the United States

While the company has retreated from growth projects in recent years to focus on its balance sheet, it will still spend about $950 million on several growth projects scheduled to come online in 2024 and 2025.

Western Central Stream

Western Central Stream (NYSE:WES) is another MLP that will significantly increase its sales this year. The company, which is approximately 45% owned by Occidental Petroleum (NYSE:OXY), forecast it would raise its base payout by 52% this year to $3.20 or more per unit. The stock currently yields 7% based on the distributions it paid out in 2023. Based on a $3.20 payout, the return would increase to 8.9%.

Western Midstream ended 2023 with a solid leverage ratio of 3.7 (defined as net debt divided by its trailing 12-month adjusted EBITDA) while also announcing the divestment of a number of non-core assets to further improve its balance sheet.

Western Midstream primarily serves Occidental Petroleum’s gathering and processing needs in the Permian of Delaware, the Powder River Basin (PRB) and the Denver-Julesburg (DJ) Basin. The Delaware Basin is often considered one of the best basins in the United States. Its low break-even prices have led to solid volume growth for the company. Western Midstream recently expanded its presence in the Powder River Basin through its acquisition of Meritage Midstream Services last fall. Production at DJ Basin has been stagnating for several years, but recently there have been signs of a turnaround.

The company is poised for solid growth with increasing Permian and PRB volumes and will spend approximately $500 million on expansion projects this year.

Energy transfer

After cutting its distribution by 50% in 2020, Energy Transfer (NYSE: ET) not only managed to bring the distribution back to pre-cut levels, but with the latest distribution increase, the company now pays a quarterly distribution a cent higher than before the payout was cut. This corresponds to a return of 7.9% for the stock. After sales are restored, the company aims to increase sales by 3% to 5% per year going forward.

In recent years, Energy Transfer has managed to significantly improve its balance sheet, reducing its debt ratio to almost four times. Once the company reaches 4x, the company expects to begin prioritizing unit repurchases. Note that Energy Transfer’s leverage refers to the leverage ratio used by the rating agency and makes adjustments for recent acquisitions.

The company has a solid payout coverage ratio of 1.9, giving it plenty of excess cash to return to shareholders once its leverage target is reached.

Similar to Western Midstream and MPLX, the company also operates a largely fee-based business, making it less directly affected by fluctuations in commodity prices. By 2024, the company expects approximately 90% of its revenue to come from paid activities. It has a very large, diversified and integrated midstream system that typically performs well across different commodity cycles.

The company has one of the best growth project portfolios in the midstream sector. The company is expected to spend about $2.5 billion in growth investments this year on a number of different expansion projects.

Three solid, high-yield options

MPLX, Western Midstream and Energy Transfer all have attractive yields and are increasing their distributions. In addition, there are predominantly fee-based businesses that are not directly influenced by raw material prices.

MPLX dividend yield data from YCharts.

Although Bill Gross is known as a bond investor, he apparently likes the money that these pipeline MLPs are throwing at investors with their distribution yields. All three stocks are solid options in the midstream space for income-focused investors to consider adding to their portfolios.

Should you invest $1,000 in Energy Transfer now?

Before buying shares of Energy Transfer, consider the following:

The Motley Fool Stock Advisor The analyst team has just identified what they think this is The 10 best stocks so investors can buy it now… and Energy Transfer wasn’t one of them. The ten stocks that made the cut could deliver huge returns in the years to come.

Think about when Nvidia created this list on April 15, 2005… if you have $1,000 invested at the time of our recommendation, You would have $533,869!*

Stock Advisor provides investors with an easy-to-understand roadmap to success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor has service more than quadrupled the return of the S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns from April 8, 2024

Geoffrey Seiler holds positions at Energy Transfer and Western Midstream Partners. The Motley Fool recommends Occidental Petroleum. The Motley Fool has a disclosure policy.

Why Billionaire Bill Gross Loves These Three High-Yield Dividend Stocks was originally published by The Motley Fool