Intel (NASDAQ:INTC) After the chip titan’s latest earnings report, shareholders are once again licking their wounds.

This is a familiar situation for Intel investors. The company has repeatedly disappointed the market by making big promises about restructuring its business, only to fail when it comes time to open the books.

This time, Intel beat estimates in the first quarter with a slight increase in revenue, but its second-quarter guidance was worse than expected as the company forecast flat revenue growth (mid-range) and a profit decline.

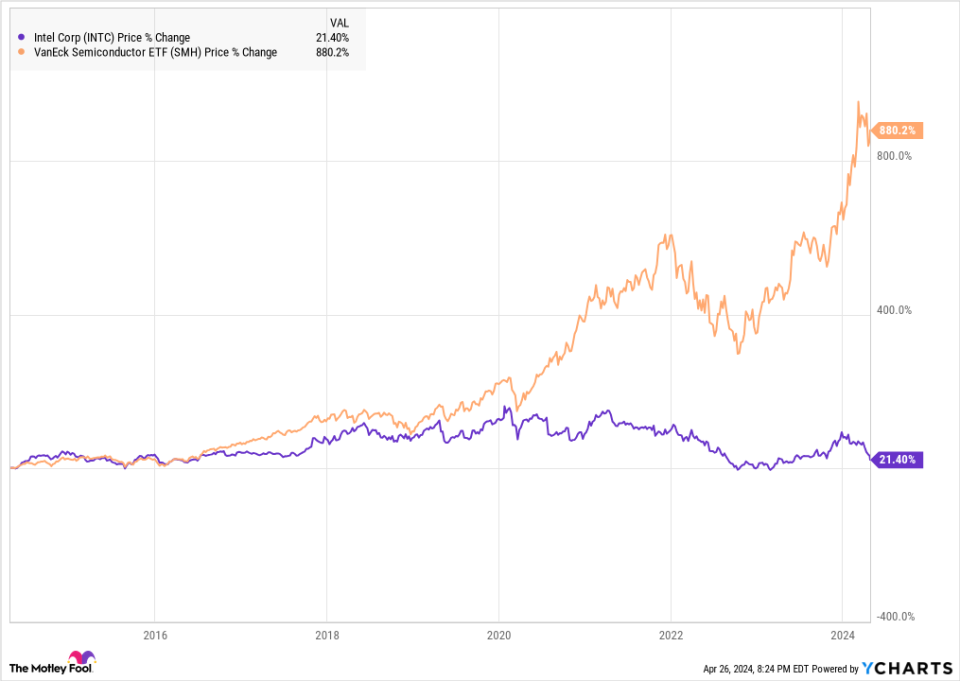

Intel stock has underperformed its peers for so long that the company’s problems run much deeper than just a quarter of its disappointing numbers. After all, the stock is still trading below its peak during the dot-com boom. Only once in the last decade has Intel’s annual revenue growth exceeded 10 percent, even when comparable to competitors Nvidia And AMD have achieved tremendous growth and returns during this time.

The following graphic shows how the performance of Intel shares compares with Van Eck Semiconductor ETFwhich has held a diversified group of chip stocks over the past decade.

While the last decade has been a picture-perfect chapter for the semiconductor industry, Intel has lost track.

There is no easy explanation for the company’s plight. Intel remains a large and generally profitable company, but it consistently lags behind its competitors.

A quote from Warren Buffett may provide the best explanation of what lies behind Intel’s chronic underperformance. The Berkshire Hathaway The boss once said to his deputies: “We can afford to lose money – a lot of money. But we cannot afford to lose our reputation – not even a hint of reputation.”

A decline in reputation is not directly reflected in the numbers, but can be an invisible reason why one competitor outperforms another. While it’s not quantifiable, the consequences over time are very real, and that seems to be part of what has plagued Intel.

Intel’s reputation problem

A variety of factors influence a brand’s reputation, including product quality, culture, corporate behavior and leadership. Reputation can influence both customer demand and employee recruitment.

A weak reputation for product quality can turn off customers, and a history of strategic failures and underperformance can also cause investors to walk away.

While Intel has long dominated the PC CPU market, the company has struggled to leverage that advantage elsewhere.

It missed the smartphone and mobile revolution. It lost ground to fabless chipmakers like AMD and has had three CEOs in the last six years, while competitors like AMD, Nvidia and Broadcom have had the same leader for a decade or more. The company also botched its position in the foundry market, having been slow to make 10nm chips and now lagging behind badly Taiwan Semiconductor And Samsung in modern chip manufacturing.

Meanwhile, Intel has spent heavily on dividends and stock buybacks throughout its history, seemingly at the expense of its core business. As the company now looks to conquer the AI GPU market, its track record offers plenty of reasons to doubt its capabilities.

Like beauty, reputation is in the eye of the beholder, and there is a wide range of opinions on Intel. These include critical arguments that argue that the company lacks innovation and is risk-averse due to its historical dominance in the PC market.

A New York Times Revelation in 2020 described a culture in which managers were complacent in the face of external competition and internally contentious as they withheld information from one another. Separate but possibly related, Apple Famously, the company ditched Intel chips in 2020 and instead installed its M1 chips in its Mac computers, allowing for longer battery life and a fanless design that helped make them quieter.

On Glassdoor, the employee review website, several commenters criticized Intel for a lack of vision, too much bureaucracy and slowness. In an industry known for “moving fast and breaking things,” these traits are clear weaknesses.

It’s worth noting that Intel’s reputation as a company is still strong. It hasn’t survived the kind of scandal that, shall we say, Wells Fargo The company did that a few years ago, but recognizing its ESG efforts is markedly different from the way potential applicants to top engineering schools or its largest customers talk about the company when making purchasing decisions.

Why Intel stocks are still best avoided

According to Intel bulls, AI and the foundry business are the two main reasons to bet on a turnaround.

However, Intel currently appears to be a loser in AI as enterprise demand shifts away from its traditional data center chips, and the company reported only 5% growth in its data center and AI segment in the first quarter. In addition, Nvidia is launching its own AI PC chip, which could take market share from Intel in its core business

Intel management said it expects more than $500 million in accelerated computing revenue from the Gaudi 3 AI chip in the second half of the year, but that’s still a small drop in the bucket since it’s about $1 % of Intel’s annual revenue.

The stock also fell a few weeks ago after the company reported a $7 billion loss in its foundry division last year. The company plans to break even in its foundry business by 2027 and achieve operating margins of 25% to 30% by 2030, but six years is an eternity in the chip sector. Intel’s own history of missed opportunities, as well as strong competition from companies like TSMC, means investors should treat this forecast with caution.

To be successful in one of these companies, the company’s reputation must be improved, and that can take a long time, as another Warren Buffett quote reminds us.

Buffett once said, “It takes 20 years to build a reputation and five minutes to ruin it.”

It may not take 20 years to restore Intel’s reputation, but investors should be skeptical of the chip giant until it proves it can innovate and compete in new markets, and it will likely take several years for that to happen makes noticeable.

Should you invest $1,000 in Intel now?

Before you buy Intel stock, consider the following:

The Motley Fool Stock Advisor The analyst team has just identified what they think this is The 10 best stocks so investors can buy it now… and Intel wasn’t one of them. The ten stocks that made the cut could deliver huge returns in the years to come.

Think about when Nvidia created this list on April 15, 2005… if you have $1,000 invested at the time of our recommendation, You would have $537,557!*

Stock Advisor provides investors with an easy-to-follow roadmap to success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks per month. The Stock Advisor has service more than quadrupled the return of the S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns from April 22, 2024

Wells Fargo is an advertising partner of The Ascent, a Motley Fool company. Jeremy Bowman holds positions at Broadcom and Wells Fargo. The Motley Fool has positions in and recommends Advanced Micro Devices, Apple, Berkshire Hathaway, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Broadcom and Intel and recommends the following options: long January 2025 calls for $45 on Intel and short May 2024 calls for $47 on Intel. The Motley Fool has a disclosure policy.

This quote from Warren Buffett perfectly explains why Intel stocks are best avoided. It was originally published by The Motley Fool