At first glance, the stock’s pullback last week makes perfect sense. Contrary to expectations, JPMorgan Chase (NYSE:JPM) did not raise its 2024 revenue forecast with first-quarter results reported on Friday. Shares subsequently fell 6%, continuing the sell-off that has been ongoing since late March. JPMorgan shares are now down 8% from that peak.

However, the proverbial glass is not half empty. It’s half full. This drop is a great opportunity to get into one of the top stocks in the financial sector at a bargain price. Here’s why.

The quarter that was and the year that won’t be

During the three-month period ending in March, JPMorgan Chase generated $42.6 billion in revenue and generated operating income per share of $4.44. Both figures were above estimates of $41.9 billion and $4.11 billion, respectively. And both were improvements over year-ago comparisons of $39.3 billion and $4.10 per share (again).

The stumbling block was leadership. JPMorgan said it expects net interest income in the region of $90 billion this year, in line with its forecast from just three months earlier. Investors expected the company to add $2 billion to $3 billion to that amount. When this didn’t happen, the market triggered a mini-revolt.

However, there are some encouraging numbers hidden in JPMorgan Chase’s Q1 numbers that support the already bullish sentiment.

JPMorgan Chase still shines

Simply put, this megabank is currently doing far better than most of its competitors.

Let’s take falling loan losses as an example. Whereas Wells Fargo (NYSE:WFC) And Citigroup (NYSE:C) While both companies have seen measurable growth in their write-offs and loss reserves, JPMorgan’s overall loan loss provision actually fell only slightly between the fourth quarter of last year and the first quarter of 2024. Write-offs and payment defaults have only increased slightly in recent quarters, but only a little bit, and most of that growth came from the credit card business. In addition, the ratio of loan loss provisions to loan portfolio remained stable last year.

It’s also worth noting that JPMorgan Chase’s interest income rose year-over-year from $20.7 billion to $23.1 billion in its most recent quarter, although the bank was unwilling to change its previous net interest income forecast for 2024 to raise. Citigroup’s net interest income rose just 1%, while Wells Fargo’s net interest income fell 8% year-over-year.

Also keep in mind that while JPMorgan Chase has not raised its interest income forecast for the current fiscal year, its expectation of net interest income worth around $90 billion in 2024 is still slightly better than its 2023 balance sheet. Growth on Meanwhile, on other fronts, any slowdown in interest income growth should be offset.

On that note, after a fairly challenging 2023 for most of the bank’s businesses, a handful of green shoots popped up in the first quarter. For example, investment banking fees improved 18% year over year and were 20% higher than the fourth quarter. Asset management revenue and even credit-based fee revenue rose in comparison.

This measurable growth precedes a potentially robust recovery in capital markets and corporate finance business in the second half of 2024. Meanwhile, the Federal Reserve reports that the entire banking industry expects increased demand for new loans this year. driven by possible interest rate cuts.

It really is Is a fortress balance sheet, and that is important

Then there are the even less obvious things, like JPMorgan’s healthy balance sheet and the strong efficiency measures that result from it.

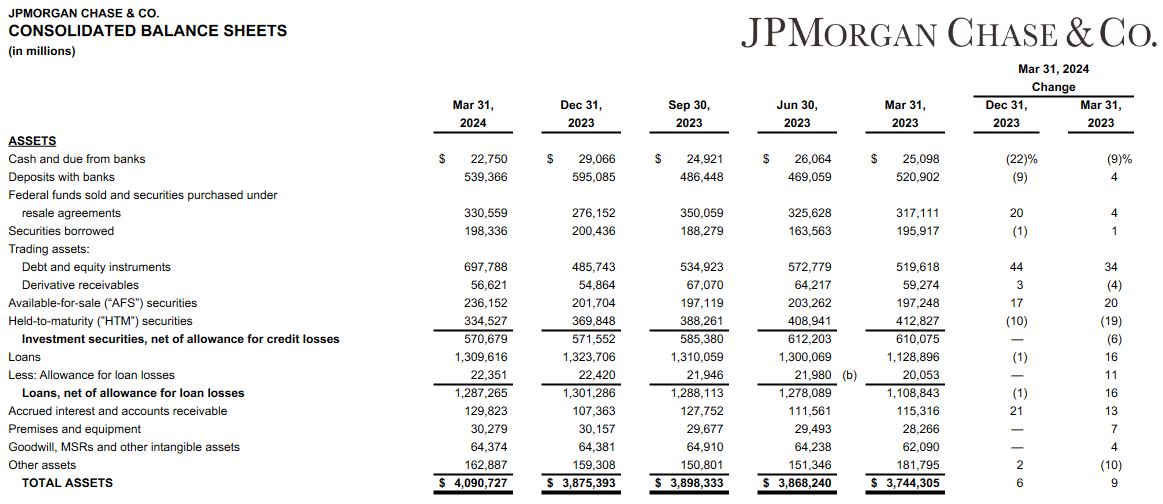

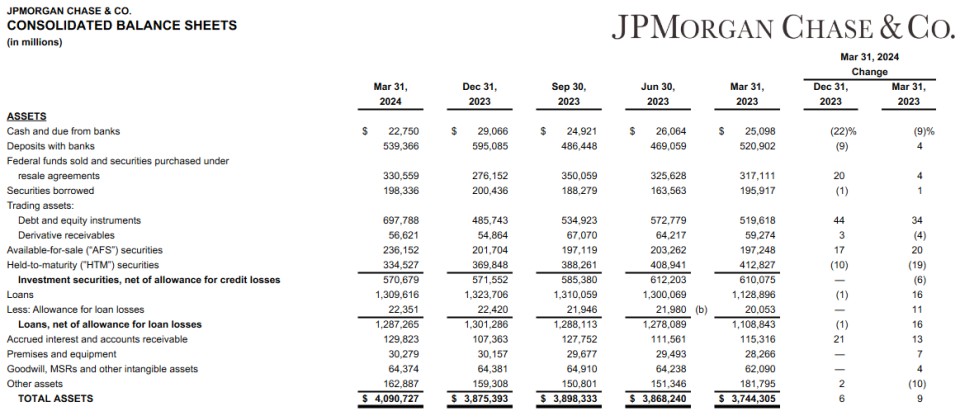

Remember last year’s collapse SVB FinancialSilicon Valley Bank and First Republic Bank? At the heart of their liquidity problems were too many long-term interest-bearing assets that were intended to be held for long periods of time (“held to maturity” or “HTM”) and too few short-term interest-bearing securities that could be sold quickly (“available for sale.” “ or “AFS”). Most banks have both types. The key is simply to find the right, balanced ratio of the two. Silicon Valley Bank and First Republic Bank did not.

To its credit, JPMorgan Chase has never faced any real liquidity threat… or Now. Nevertheless, the bank was able to reduce its less liquid HTM holdings and increase its AFS securities. This gives the bank a significantly higher degree of tax flexibility if necessary.

With that in mind, what the company calls its “fortress balance sheet,” so to speak, is currently capable of weathering $520 billion in losses without breaking the bank.

However, it is about more than just having enough liquid assets. The solid balance sheet ultimately leads to more efficient and profitable use of these assets. JPMorgan’s return on total equity (ROE) was 17% in the first quarter, while its return on tangible common equity (ROTCE) reached 21% in the recently completed quarter. For comparison, Wells Fargo’s ROE fell to 10.5% in the first quarter, while ROTCE fell to 12.3% last quarter from 14% a year ago. Citi’s comparable figures for the quarter are 6.6% and 7.6%, respectively.

JPMorgan Chase stock is a top pick worth buying now

Of course, companies are more than just numbers. Like people and pets, they all have their own personalities. That can make a difference in the performance of their stocks. JPMorgan is no exception to this reality.

Yet truly great companies consistently achieve objectively healthy financial results. JPMorgan Chase has been doing exactly that for years and is still doing it.

Take the hint. This is one of the strongest names in the financial sector, if not one the strongest. The stock’s post-earnings decline is a buying opportunity, even if the exact bottom has not yet been reached. They’ll step in while the stock price is about 12 times this year’s earnings estimates and the yield is just over 2.3%.

Should you invest $1,000 in JPMorgan Chase now?

Before you buy JPMorgan Chase stock, consider the following:

The Motley Fool Stock Advisor The analyst team has just identified what they think this is The 10 best stocks so investors can buy it now… and JPMorgan Chase wasn’t one of them. The ten stocks that made the cut could deliver huge returns in the years to come.

Stock Advisor provides investors with an easy-to-follow roadmap to success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks per month. The Stock Advisor The service has more than tripled the returns of the S&P 500 since 2002*.

Check out the 10 stocks

*Stock Advisor returns from April 8, 2024

Citigroup is an advertising partner of The Ascent, a Motley Fool company. SVB Financial provides lending and banking services to The Motley Fool. Wells Fargo is an advertising partner of The Ascent, a Motley Fool company. JPMorgan Chase is an advertising partner of The Ascent, a Motley Fool company. James Brumley has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends JPMorgan Chase. The Motley Fool has a disclosure policy.

Is JPMorgan Chase Stock a Buy on This Drop? was originally published by The Motley Fool