Intel (NASDAQ:INTC) was once the world’s leading chipmaker. The company dominated the central processing unit (CPU) market and had lucrative partnerships with tech titans like Apple. However, a series of missteps and market changes caused Intel shares to plunge 46% over the past three years.

In recent years, the company has experienced several quarters of declining sales while simultaneously shrinking market share in the chip sector. Intel has finally returned to revenue growth, posting gains in the fourth quarter of 2023 and the first quarter of 2024. Nevertheless, investors remain cautious about the stock. Emerging competitors like Nvidia And modern micro devices threaten Intel’s future in emerging markets such as AI.

However, the company is trying to differentiate itself from these chipmakers by adopting an internal foundry model similar to Taiwan Semiconductor Manufacturing Company operates. It will take time for Intel to see significant earnings growth through this transition, but it might be worth investing in the company at one of its lowest positions to capitalize on its potential comeback.

For this reason, Intel stock is a buy for investors who are willing to hold it for the very long term.

A dark quarterly publication

On April 25, Intel reported its first-quarter 2024 results. During the quarter, revenue rose 9% year-over-year to $13 billion, but missed analysts’ forecasts by about $80 million. Non-GAAP (adjusted) earnings per share (EPS) were $0.18, beating expectations by $0.04.

However, the growth and better-than-expected EPS weren’t enough to entice investors, as Intel shares fell 14% since its first-quarter results were released.

Intel disappointed with weak forecasts for the current quarter (Q2 2024). For the second quarter, the company expects earnings of $0.10 per share on revenue of $13 billion. By comparison, Wall Street expected earnings per share of $0.25 and revenue of $13.6 billion.

Intel CEO Pat Gelsinger reiterated the company’s long-term potential, saying: “We are one of two, maybe three companies in the world that can continue to enable next-generation chip technologies.” Taiwan Semi is the other obvious name on its list , followed by a “maybe” for Samsung.

The first quarter of 2024 included revenue from Intel Foundry, its new manufacturing division, for the first time. The segment reported revenue of just over $4 billion, down 10% year-over-year. Meanwhile, operating losses were $2.5 billion, compared to losses of $7 billion reported in 2023.

However, Counterpoint analyst Akshara Bassi points out: “Operating a foundry is a capital-intensive business. For this reason, most competitors are fabless companies and are happy to outsource the work to TSMC.” Intel expects foundry losses to peak in 2024 and break even by the end of 2030.

Intel is moving in the right direction, but the stock requires patience

Intel’s transition to a foundry-first company will be costly. However, the company expects the change will help reduce costs and save between $8 billion and $10 billion by 2025. Meanwhile, Intel is expected to achieve non-GAAP gross margins of 60% through greater efficiency.

Additionally, Intel won’t be alone in covering the costs of its foundry business. The company is a leading recipient of President Biden’s CHIPS Act, an initiative to expand the United States’ semiconductor manufacturing capacity. The program includes $8.5 billion to build at least four facilities across the country.

The distribution of government money has already begun, and the Biden administration announced in April that Samsung would receive just over $6 billion to expand its chip production capacity. The initiative is still in its infancy. Experts believe it will take 2027 or 2028 for U.S.-made chips to make their way into the mainstream consumer space. However, it is a promising direction for Intel.

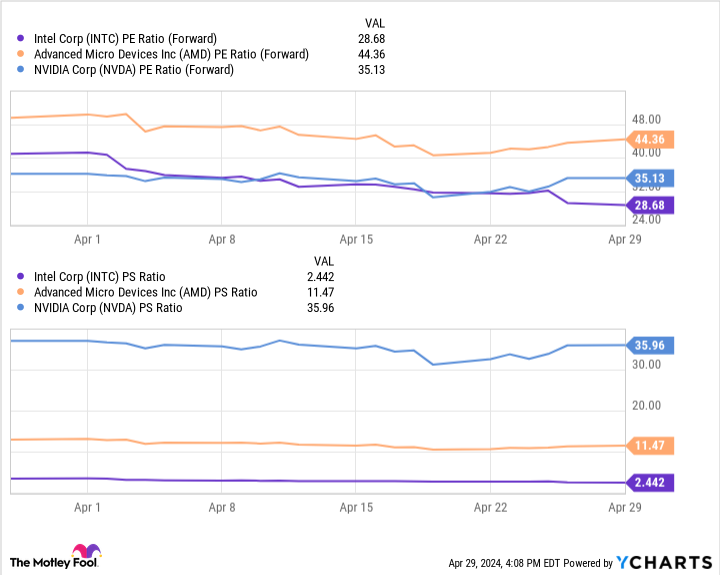

Perhaps the only positive development in Intel’s falling stock price is that Intel’s stock may be the best valued option in the chip market. Nvidia and AMD’s recent rallies have sent their stock prices soaring over the last year.

The chart above shows that Intel has by far the lowest price-to-earnings and price-to-sales ratios of these three chipmakers. These numbers suggest that Intel stock is trading cheaper compared to AMD or Nvidia.

Therefore, anyone looking to add a chip stock to their portfolio would probably be wise to make a long-term investment in Intel now while waiting for Nvidia and AMD to reach a more attractive price.

Should you invest $1,000 in Intel now?

Before you buy Intel stock, consider the following:

The Motley Fool Stock Advisor The analyst team has just identified what they think this is The 10 best stocks so investors can buy it now… and Intel wasn’t one of them. The ten stocks that made the cut could deliver huge returns in the years to come.

Think about when Nvidia created this list on April 15, 2005… if you have $1,000 invested at the time of our recommendation, You would have $544,015!*

Stock Advisor provides investors with an easy-to-understand roadmap to success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor has service more than quadrupled the return of the S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of April 30, 2024

Dani Cook has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Apple, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Intel and recommends the following options: long $45 January 2025 calls on Intel and short $47 May 2024 calls on Intel. The Motley Fool has a disclosure policy.

Is Intel stock a buy? was originally published by The Motley Fool