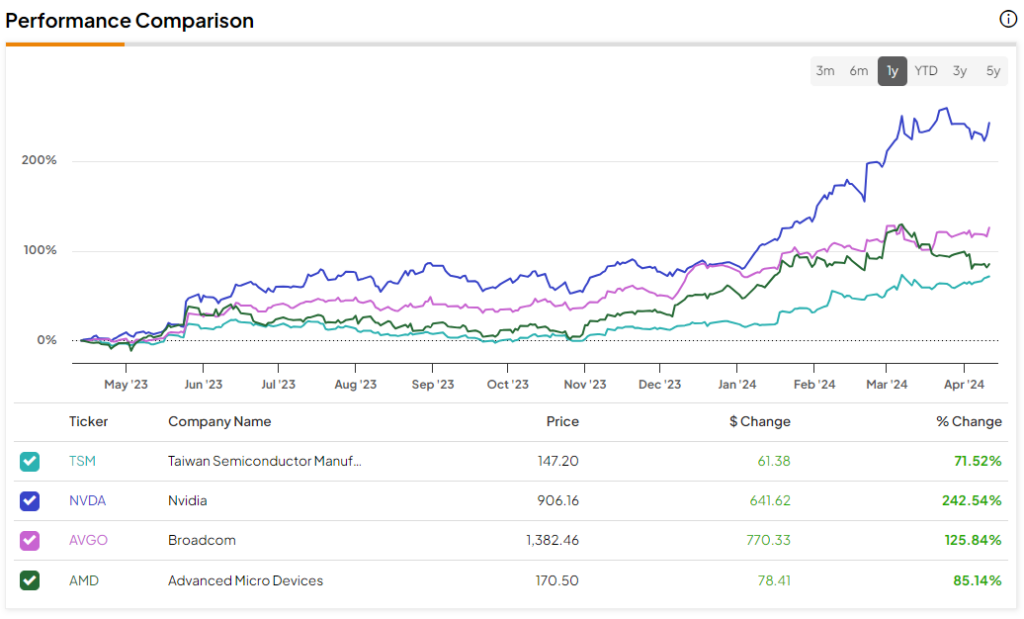

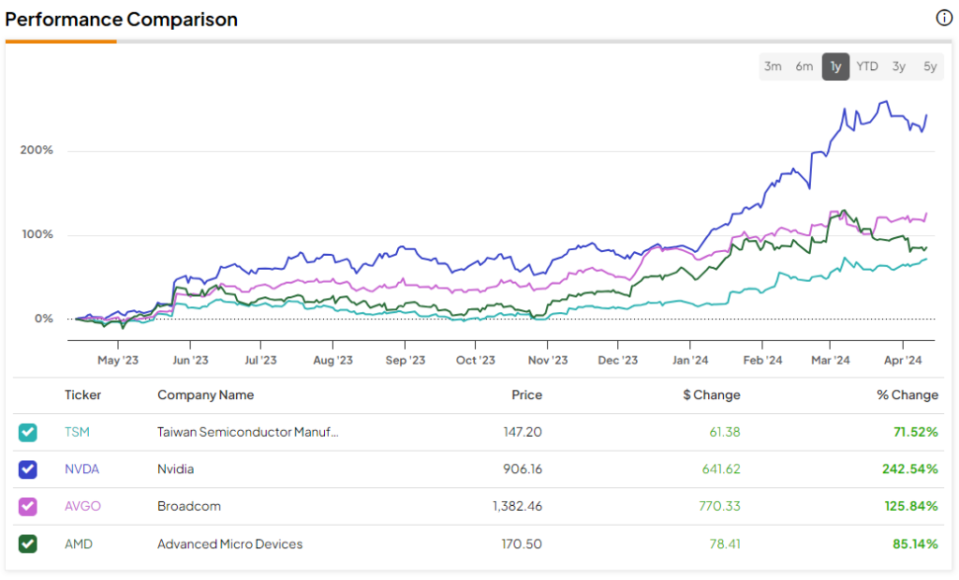

Taiwan semiconductor manufacturing (NYSE:TSM), the world’s largest chipmaker, recently reported impressive sales figures for March. In particular Nvidia (NASDAQ:NVDA), which has gained 242.5% in the past year, relies on TSM for chip manufacturing. However, the performance of TSM shares (plus 71.5% over the same period; see comparison image below) was relatively muted. This begs the question: Can TSM replicate NVDA’s outstanding performance? The answer is probably yes.

Given the ongoing AI boom, increased funding from the US and an attractive valuation, TSM looks like a compelling buy at the moment.

Preliminary earnings numbers suggest a positive outlook for upcoming earnings

On April 10, TSM unveiled impressive March revenue figures, posting 34.3% year-on-year growth, the highest monthly growth since November 2022, to a total of 195.2 billion New Taiwan dollars (approximately $6.1 billion). Additionally, first-quarter revenue is expected to rise 16.5% year-over-year to 592.6 billion New Taiwan dollars (around $18.4 billion).

It’s worth noting that TSM expects revenue growth of mid-20% for fiscal 2024, driven by strong demand for its latest nanochips amid the AI boom. Furthermore, the company reiterated in January 2024 that its AI revenues are growing rapidly at around 50% per year. This confirmation is particularly reassuring after reporting a decline in sales in 2023.

TSM manufactures the chips and supplies them to technology giants such as Nvidia, Advanced Micro Devices (NASDAQ:AMD) and Apple (NASDAQ:AAPL). Ahead of the first-quarter earnings release, expected on April 18, let’s take a look at what the future holds for TSM.

The AI revolution will drive growth at TSM

The AI revolution has taken the world by storm. I am firmly convinced that the growth path will continue. The AI industry, still in its infancy, is expected to witness remarkable expansion across various industries and applications. Accordingly Next Move strategy consultingThe industry is expected to grow into a $1.85 trillion behemoth by 2030, up from around $208 billion in 2023.

TSM’s customers rely heavily on the company to produce the chips they develop. An uproar in demand for everything AI-related has led to huge demand for AI chips.

To add to the AI growth push, TSM received a further boost to its manufacturing operations as the company received approval for $11.6 billion in direct federal funding under the US government’s CHIPS Act. The company will receive $6.6 billion in grants to expand its manufacturing facility in Phoenix, Arizona. Additionally, TSM is eligible for an additional $5 billion loan.

TSM has already invested in building two factories at the site and will use the financing to build another factory. The company’s total investment across all three factories is estimated at $65 billion. This is the “largest foreign direct investment in a greenfield project in U.S. history,” the press release states.

TSM plans to produce chips with 2-nanometer technology in the second factory from 2028. In the coming years, TSM is expected to benefit from massive investments that will significantly improve its production processes and bring in the latest technological advances.

TSM Chairman Mark Liu expressed optimism, stating: “Our US operations enable us to better support our US customers, which include several of the world’s leading technology companies.” Our US operations will also expand our ability to provide future “To drive advances in semiconductor technology.”

To date, the majority of TSM’s production capacity is located in Taiwan, which poses geographical risk (potential threat of Chinese invasion, earthquakes, etc.). The recent expansion announcement mitigates this risk. With the expansion of production in the US, TSM will likely be able to serve its blue-chip US-based customers such as Nvidia, AMD and Apple more efficiently. Additionally, record-high crypto prices are leading to higher demand for chips, boosting TSM’s growth prospects.

TSM is trading at a cheap valuation

From a valuation perspective, TSM looks cheap. The company is currently trading at an attractive price-to-earnings ratio of 23x compared to significantly higher multiples of its peer group. Semiconductor company Advanced Micro Devices trades at a higher forward P/E ratio (49x), while AI wunderkind Nvidia trades at a forward P/E ratio of 36.4x.

Wall Street analysts expect TSM’s earnings per share to reach $9.02 in fiscal 2026. If TSM maintains the same forward P/E ratio until then, the share price will be around $207, or 45% above the current price. Therefore, given the strong growth potential in the AI space, it makes sense to consider buying TSM stock at current levels.

Is TSM Stock a Buy According to Analysts?

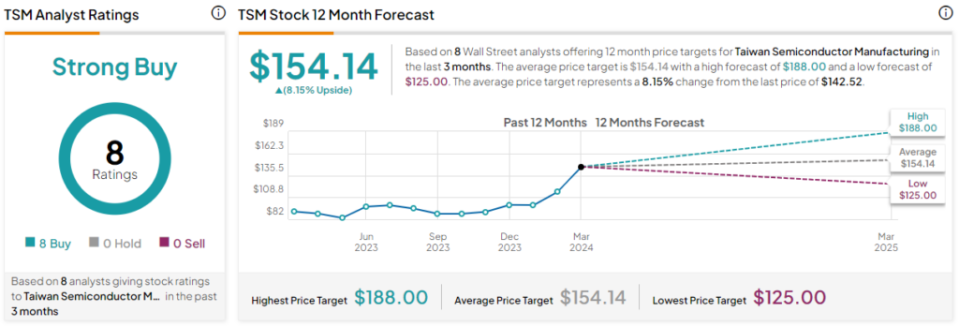

The Wall Street community is clearly bullish on Taiwan Semiconductor Manufacturing stock. Overall, the stock has a Strong Buy consensus rating based on eight unanimous Buys. TSM stock’s average price target of $154.14 implies an upside potential of 8.2% from current levels.

Conclusion: TSM offers a strong opportunity for long-term growth

The semiconductor industry is experiencing a significant upswing, largely due to the AI boom. TSM, along with its AI-focused peers, will benefit from this relentless demand. With strategic investments and expansion plans to meet future demands, TSM appears well-positioned for sustainable growth. Taking these factors into account, I am inclined to buy the stock at its current levels as I expect long-term benefits from its AI potential.

Disclosure